.jpg?ph=8f1064689b)

About:

Employees (Teachers) who have recruited on or after 01.09.2004 have to come under the New Contributory Pension Scheme. For this, the employees have to deduct 10% of their Basic Pay & D.A towards their contribution and Government will add the same amount to their accounts. D.A arrears and other arrears of these employees will be credited to the C S S (Compulsory Savings Scheme). Now our State Government has entered into an agreement with N S D L (National Security Depositories Limited), Bombay to maintain PRAN accounts as Central Record Keeping Agendy ( C R A). Now, all the employees coming under the C P S have to apply for P R A N (Permanent Retirement Account Number) alloted & maintained by N S D L, Bombay. For this, N S D L has appointed KARVY Consultants as Facility Centre, and there are two Facility Centres

1. at Hyderabad and 2. at Visakhapatnam. Here, GOs, Memos, Proceedings and relevant informatin on C P S are provided.

|

1-Address of Karvy Consultants Hyderabad:

HYDERABAD - KARVY CENTREKARVY CENTRE, 8-2-609/K, Road #10, Banjara Hills HYDERABAD Andhra Pradesh ,India PIN CODE: 500034 PHONE : 040 66282814 040-44677527 040-23312454 EMAIL : mailmanager@karvy.com |

NEW APPLICATIONS:

NEW APPLICATIONS:- Form S1-Application for allottment of PRAN

- DDO Covering Letter for Subscriber Registration

- DDO Registration Form

- Treasury Covering Letter

Online Links Useful for CPS/PRAN

-

Government Orders on CPS Scheme

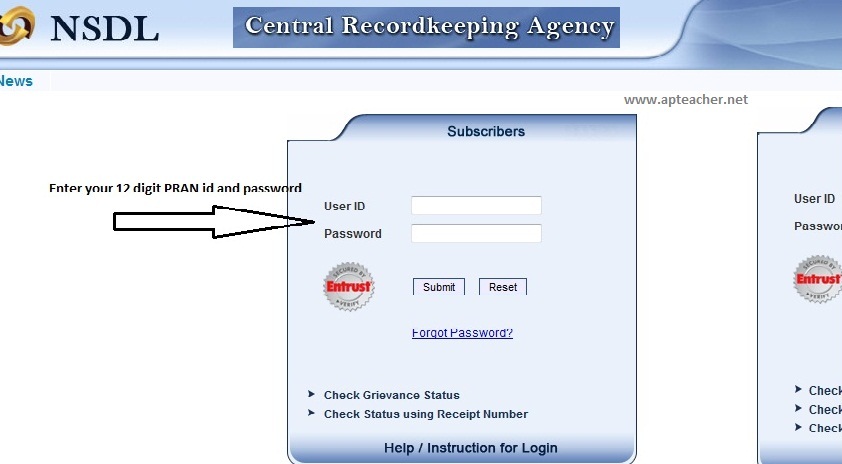

- CPS Subscribers Login Using their User ID and Password-Click Here

- New Pension Scheme (NPS) Official Website-Click Here

- Have you applied for PRAN Number-Then Track the Status of PRAN Allotment Using your Acknowledge Number given at the time of Registration-Click Here

- Track the IRA Status of PRAN Using Your Treasury ID Click Here

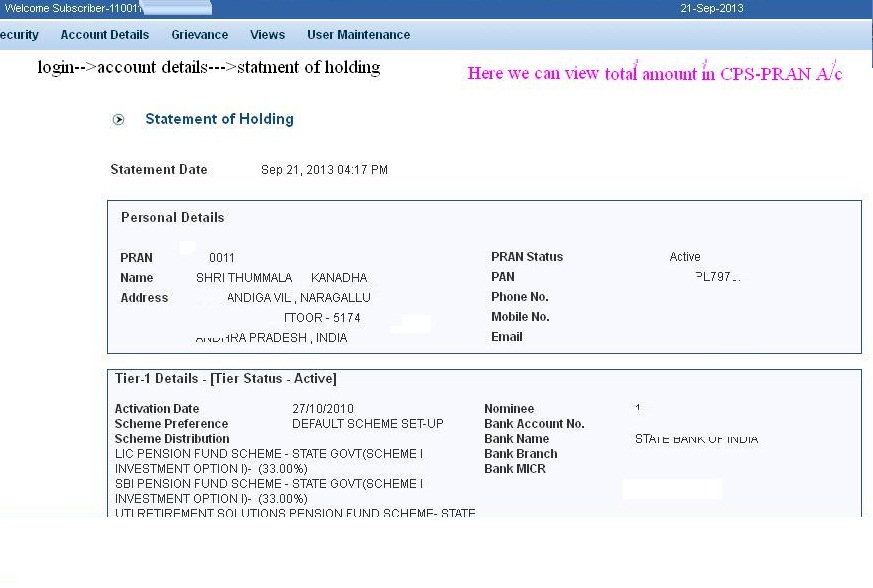

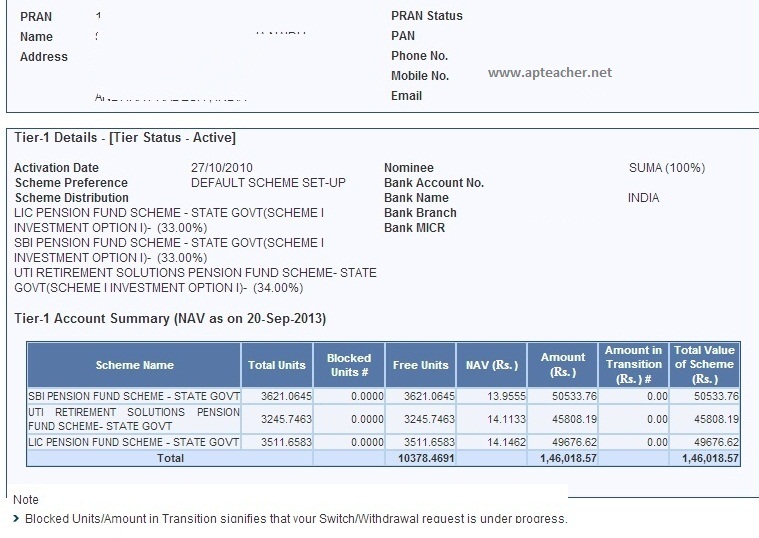

- Latest Fund Values of CPS-Click Here

MODIFICATION FORMS FOR REGISTERED SUBSCRIBERS:- Subscribers Change Details Form

- Subscribers Photo and Signature Change

- Covering letter of DDO for change in Photo and Signature

CPS RELATED MEMOs & GOs: - GO.226 29/9/11- 8% Interest on CPS Contributions from 1.9.04 to 31.3.11

- All GOs issued by Govt of AP relating to CPS (GO.653, 654, 655)

- Memo No.16047 2009 dt.26.10.10

- Memo No.D2 10393 2008 dt.10.11.08

- DO Lr No.16047 2009 dt.25.2.09

USEFUL CPS/NPS LINKS :- OFFICIAL WEBSITE OF NEW PENSION SCHEME (NPS)

- Track the status of PRAN Card

- Track the status of PRAN Application with Ack Id

- Track the STATUS of REGISTRATION Using Receipt No

- CPS-Check your fund Value-Enter Your Id and Password from PRAN

- Track the Latest NAVs of CPS Funds

- Clarifications on NPS Scheme Details

- Clarifications on NPS Contributions

| Know about New Pension System Trust by PFRDA |

- In pursuant to the advice of the Central Government vide letter D.O. No 5(75)/2006-ECB & PR dated 24th April 2007; The NPS Trust was established by PFRDA on 27th February, 2008 with the execution of the NPS Trust Deed and the Board of Trustees of NPS Trust was formed with three members to begin with. Subsequently three more Members were included in the Board. The term of the Trustees is for two years. Sh. N.R.Rayalu was also appointed CEO also of the NPS Trust on his retirement as Dy CAG, Government of India w.e.f 12th June 2008

1. Sh Yogendra Narain Chairman

2. Sh.N.R.Rayalu Trustee & CEO

3. Sh. Umraomal Purohit Trustee

4. Sh.G.N.Bajpai Trustee

5. Sh.Naresh Dayal Trustee

As part of its obligations, the NPS Trust ensures that:-

- the PF(s) has been diligent in empanelling the brokers, in monitoring securities transactions with brokers and avoiding undue concentration of business with any broker;

- the PF(s) has not given any undue or unfair advantage to any associates or dealt with any of the associates of the Pension Fund in any manner detrimental to interest of the beneficiaries

- the PF(s) has been managing the Fund Schemes independently of other activities and has taken adequate steps to ensure that the interests of the beneficiaries are not compromised;

- all the activities and the transactions of the PF(s) are in accordance with the provisions of the PFRDA guidelines/directions.

- To begin with the NPS was operational for the Central Govt Employees (except defense forces) joining the service on after 1.1.2004. Subsequently the State Governments have also started joining the NPS. Three Fund managers as mentioned below were appointed to manage the Funds of the Government employees with effect from 1.1.2008.

- SBI Pension Funds Private Limited

- UTI Retirement Solutions Limited

- LIC Pension Fund Limited

- SBI Pension Funds Private Limited

- UTI Retirement Solutions Limited

- ICICI Prudential Pension Funds Management Company limited

- Kotak Mahindra Pension Fund Limited

- IDFC Pension Fund Management Company Limited Reliance Capital Pension Fund Limited

Agreements with all the Pension Fund Managers have been signed. Agreement has also been signed with the Stock Holding Corporation of India who acts as custodian of investment Instruments. So far thirteen State Governments /UT have joined the NPS by signing the agreement with the NPS Trust. More State Governments have shown their inclination to join the NPS Architecture.

A quarterly review of the Pension Fund managers is carried out by the NPS Trust to review and evaluate the performance of the Fund Managers and make suggestions for improvement.

A quarterly review of the Pension Fund managers is carried out by the NPS Trust to review and evaluate the performance of the Fund Managers and make suggestions for improvement.

ఉపాధ్యాయమిత్రులు ఉచితమెస్సేజ్ల కొరకు మీ మొబైల్ నుండి SMSచేయండి

FOLLOW STUNELLORE అని టైప్ చేసి 9219592195 నంబరుకు SMS పంపండి

IF Forgot your I CPS PRAN I PIN RESET NOW PROCESS

CPS/PRAN PASSWORD RESET | CRA.NSDL CPS/PRAN PASSWORD FORGOT-RESET AGAIN | NSDL IS ALLOWING TO RESET PASSWORD FOR YOUR CPS/ PRAN ACCOUNT | PASSWORD FOR CPS/PRAN CAN BE RESET THROUGH CRA.NSDL WEBSITE

https://cra-nsdl.com/CRA/ is fecilitating to reset our CPS/ PRAN Password | Process to reset our Password for CPS/PRAN Account So many of us including me are facing problem to view CPS statement because we forgot our password and there was no chance to reset our password and most of us gave up it. But for last some days CRA.NSDL is allowing us to reset our password by ourself online and no need to approach Nodal office by fiiling any form. Here is the Process.

STEP BY STEP PROCESS TO RESET CPS/PRAN PASSWORD:

- Click Here There we find two boxes as Subscribers and Nodal Office

- In Subscibers box we have to enter our PRAN Number where we see User Id and Click on

- Forgot Password It will take us to another window, there we see " Reset Password using secret question" and " Instant Reset I-PIN"

- There we select " Instant Reset I-PIN " and again it will take us to the page where we can change password

- There we have to give all the Mondatory aspects and also a password u wish

- Password should be like sandhya@143 (namesimbol number) and have to conform in the next column

- After filling the mondatory fields ( * Marked Fieldsare Mondatory) click on Generate OTP

- An One Time Password ( OTP) comes to our Registered Phone Number

- Enter the OTP at asked place then there willappear a message Successfully completed

- Again u go to OR 15 CPS Fund Value Page Click Here

- There u enter your PRAN Number and your password you have give there.

- You will enter to your PRAN Account and you will be asked to reset password again

- Reset your password as explained

- Congratulations you have Successfully reset your CPS/PRAN Password