.jpg?ph=8f1064689b)

On 13th Jan 2015, JAC Joint Action Committee of Employees, Teachers, Workers and Pensioners, Andhra Pradesh has wrote a letter to the Convener of Group of Ministers on PRC

Ref:- Govt. Lr. No. 247/01/A1/HRM.V/2015-3, Fin. (HRM.V) Dept., dated 08.01.2015.

Ref:- Govt. Lr. No. 247/01/A1/HRM.V/2015-3, Fin. (HRM.V) Dept., dated 08.01.2015.

- The Hon'ble Minister for Finance has convened a meeting with the Employees Associations on Implementation of the 10th PRC at 2.00 P.M. on 13.01.2015 in the Chambers of Minister for Finance & Planning, A.P. Secretariat.

- In this connection, JAC has discussed the matter in detail in the JAC Executive Committee Meeting held on 12.01.2015 at APNGO's Home, Hyderabad and decided to discuss with the Group of Ministers on the following issues.

JAC Demands on PRC 2014

- 1) Minimum Pay has to be raised from Rs.13,000/- to Rs.15,000/- and maximum pay from Rs. 1,10,850/- to 1,37,600/-.

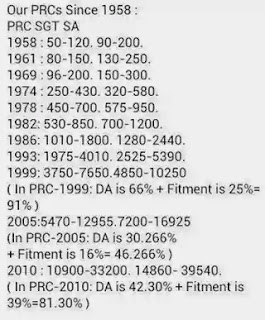

- 2) The JAC expressed dissatisfaction on the recommendation of 29% Fitment by the PRC. The JAC is of the opinion that 69% is appropriate to the present inflation rates.

- 3) The PRC has to be implemented w.e.f. 01.07.2013 with all monetary benefits.

- 4) The services of Contract employees and Full Time Contingent Workers has to be regularised.

- 5) The HRA payable with in peripheral distance of 8 Kms. has to be enhanced to 15 Kms.

- 6) The maximum Increment rate of 2.33% has to be raised to 2.832%.

- 7) Gratuity has to be enhanced up to Rs.15.00 Lakhs instead of Rs.12.00 Lakhs.

- 8) Restoration of Commuted portion of Pension paid after 12 years instead of present 15 years.

- 9) District Headquarters, viz., Machilipatnam, Sr'ikakulam & Chittoor have to be allowed HRA@ 20% irrespective of Population.

- 10) The Bad Climate Allowance for the employees working in Agencies has to be restored.

- 11) The Pay Scales of Common Categories, i.e., Junior Asst., Senior Asst., Superintendent has to be raised on par with Secretariat Staff since the qualifications and work nature are one and the same.

- 12)180 days Maternity leave to the Contract and Outsourcing employees has to be provided with Pay and Allowances.

- 13) All employees who are drawing salary from Government has to be provided salaries under 010 Head of Account duly bringing under roof by changing system of Grant-in-Aid etc.

- 14) The Pay Revision has to be implemented to all State Govt. Employees including Public Sector Undertakings and Gurukula Vidyalayas, Co-operative Societies etc.

- 15) The superannuation age to State Govt. employees has to be extended to all State Govt. Organisations like Public Sector, Grandhalaya Samsthas, Gurukulas. Societies etc.which were not already enhanced.

- 16) School Fees reimbursement has to be paid on par with Govt. of India rates.